Article Archives

Article Categories

Articles

The Speed Trap

AI-Fueled Data Center Growth Meets Building Lifecycle Reality

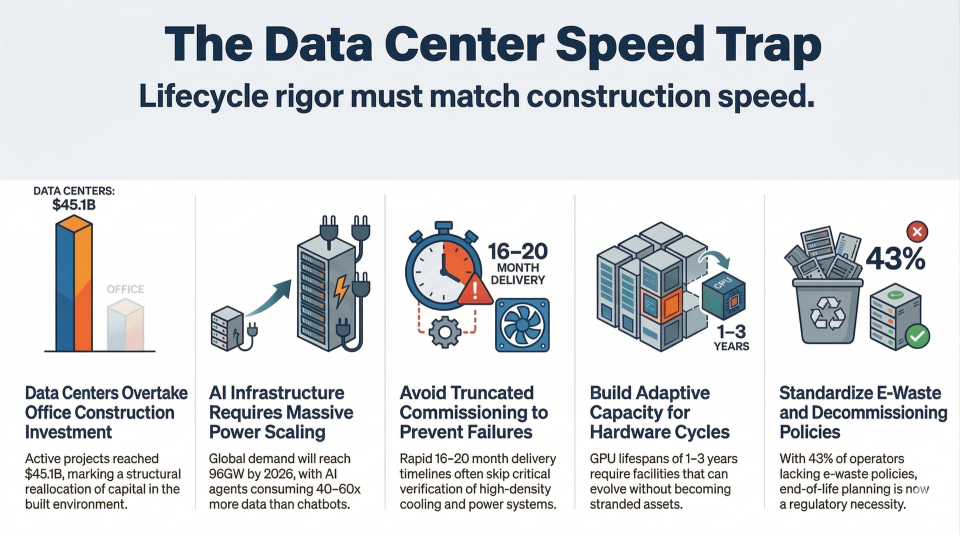

For the first time in U.S. history, investment in new data center construction has surpassed investment in new office buildings. At $45.1 billion in active projects - a 228% surge since the launch of ChatGPT in late 2022 - the data center sector is reshaping where capital flows within the built environment. Office construction, by contrast, has declined 38% over the same period to $43.5 billion. This is not a cyclical blip. It is a structural reallocation of the economy.

REIT markets have priced in the shift decisively. Data Center REITs delivered a +24.33% year-to-date return through February 2026, trading at a 26.9x price-to-FFO multiple - the least-shorted property type in the sector. Office REITs, at -8.17% YTD and a 7.3x multiple, sit at the opposite end of the spectrum. The 3.7x valuation gap between these two asset classes tells a story of irreversible market repricing.

But here is the question the market has not fully priced: can the industry build this fast without creating a lifecycle deficit that compounds for decades?

The Numbers at a Glance

What Is Driving the Surge

The demand thesis is not speculative - it is structural. At Nvidia’s GTC 2026 keynote, Jensen Huang declared the year an “inflection point for inference,” unveiling hardware that integrates Groq technology with traditional GPU architecture for faster, more efficient inference at scale. The implication is clear: the compute infrastructure required for AI is not a one-time buildout. It is a continuously escalating demand curve.

Alibaba’s analysis puts the scale in perspective: autonomous AI agents consume tokens at 40–60x the rate of traditional chatbots. As enterprises move from pilot programs to production-scale agent deployments, the demand floor rises accordingly. Critical power to support global data center operations is expected to nearly double between 2023 and 2026, reaching approximately 96 gigawatts - with AI operations alone consuming over 40% of that power.

Regional grid operators are already sounding alarms. PJM projects a 6-gigawatt shortfall by 2027 - equivalent to the output of six large nuclear plants. Approximately 70% of the existing U.S. power grid is approaching end-of-life, creating a collision between surging demand and aging infrastructure.

The Lifecycle Gap: What Speed Leaves Behind

Building fast is not the same as building well. Modular construction techniques have compressed data center delivery timelines by 30–50%, bringing some projects to completion in 16–20 months. That is an extraordinary engineering achievement. But speed optimizes for one phase of the building lifecycle - delivery - while potentially shortchanging the phases that follow: operations, maintenance, adaptation, and decommissioning.

Think of it like a Formula 1 pit stop. The car gets back on the track in record time, but if the mechanics skip a lug nut, the consequences emerge at 200 miles per hour. In data centers, the “lug nuts” are the lifecycle considerations that do not appear on the construction schedule but determine whether a facility remains viable, efficient, and safe over its intended service life.

Likely Lifecycle Omissions in Rapid Development Cycles

Commissioning Depth

Compressed schedules often truncate commissioning - the systematic process of verifying that every system performs as designed. In a 50+ megawatt facility running at rack densities of 30–50 kW, the margin for error in power distribution, cooling redundancy, and failover sequencing is razor-thin. Incomplete commissioning does not cause immediate failure; it creates latent risk that surfaces during the first major stress event.

Maintainability-by-Design

When delivery speed is the primary metric, design decisions that optimize long-term maintainability - adequate service corridors, accessible mechanical systems, modular component replacement paths - can be deprioritized. Facilities designed for construction speed may prove expensive to operate and difficult to service, particularly as power densities continue to climb.

Adaptive Capacity

Customer specifications shift mid-deployment as AI hardware evolves faster than buildings can rise. NVIDIA’s shift to an annual product cadence - Hopper (2022), Blackwell (2024), Rubin (2026) - means the computing hardware inside a facility may turn over every 1–3 years. A building designed for today’s thermal profile may be inadequate for next year’s GPU generation. Facilities that lack adaptive capacity become stranded assets in all but name.

Decommissioning and End-of-Life Planning

With GPU functional lifespans as short as 1–3 years and hardware refresh cycles accelerating, data centers will generate unprecedented volumes of electronic waste. Yet 12% of data centers engage in no e-waste recycling, and 43% lack an environmental policy for e-waste management. European Commission regulations now require detailed sustainability reporting for data centers with a capacity of over 500 kW, with similar frameworks emerging globally. Operators who defer decommissioning planning to “later” will find that “later” arrives on a very short timeline.

Workforce Development

Single data center campuses now require 4,000 construction workers, up from 750 a few years ago. The operational side faces parallel pressure: facilities running liquid cooling at 50 kW per rack demand specialized expertise that the traditional FM workforce was not trained to deliver. The pipeline of qualified data center operations professionals has not kept pace with the build rate.

Key Takeaways

For Commercial Real Estate

- The capital migration from office to data center is structural, not cyclical. The 228% construction surge versus a 38% office decline represents a permanent reallocation of investment in the built environment.

- Valuation premiums reward operators who deliver capacity, but lifecycle risk is not yet priced. Investors should evaluate not just delivery speed but long-term operational resilience and adaptive capacity.

- Stranded-asset risk is real. A facility designed for 2026 thermal loads may be functionally obsolete for 2028 hardware without significant retrofit investment.

For Energy Capacity and Distribution

- Data center power demand is projected to reach 75.8 GW in the U.S. alone by 2026. Over 60% of this power still comes from fossil fuels, despite renewable pledges.

- Grid infrastructure is simultaneously aging and overloaded - 70% of the U.S. grid is approaching end-of-life, and regional operators project multi-gigawatt shortfalls.

- Operators are evolving from passive energy consumers to active grid stakeholders, co-investing in infrastructure upgrades, deploying on-site generation, and enabling demand-response flexibility.

For Operations and Maintenance

- The shift from 5–8 kW to 30–50 kW rack densities transforms every aspect of facility operations - cooling strategies, power distribution, redundancy engineering, and maintenance protocols.

- Predictive maintenance powered by AI and condition-based monitoring is replacing traditional interval-based approaches, but implementation requires investment in sensors, data infrastructure, and skilled personnel.

- The FM profession faces a pivotal moment: declining office portfolios are compressing the traditional market, while data center operations are creating demand for specialized expertise that commands premium compensation.

The Bottom Line

The data center buildout underway is historic in scale and speed. The market signals are unambiguous: capital is flowing, valuations are rising, and demand has a structural floor that continues to rise. But the building lifecycle does not negotiate with construction schedules. A facility that is commissioned incompletely, designed without adaptive capacity, and operated without a decommissioning strategy is not a long-term asset - it is a depreciating liability with excellent curb appeal.

The industry has an opportunity to get this right: to match the speed of delivery with the rigor of lifecycle planning. The organizations that do - integrating commissioning depth, maintainability-by-design, adaptive infrastructure, and end-of-life stewardship into every project - will own the next decade. Those who treat lifecycle management as an afterthought will discover, at great expense, that the fastest to build is not always the best.